5. The new sustainability reporting framework

In the survey and in this report, the term sustainability reporting refers to a report prepared in accordance with the ESRS. The survey did not concern information presented on the basis of Article 8 of the Taxonomy Regulation1, because the Taxonomy Regulation is already in force.

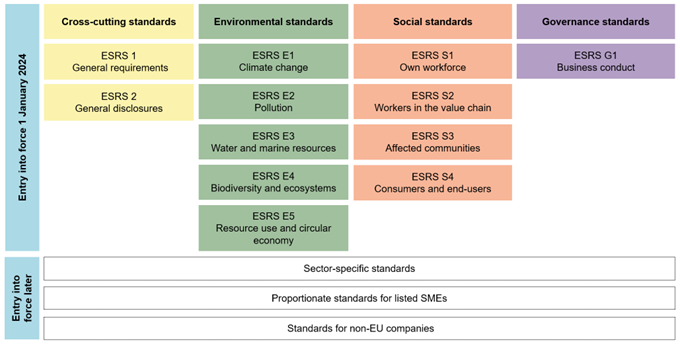

Figure 5. New European Sustainability Reporting Standards (ESRS) as part of EU legislation

Source: Commission Delegated Regulation (EU) C(2023) 5303 final 31 July 2023. Figure: Financial Supervisory Authority

Since 2017, the Accounting Act has obliged certain companies to provide a report on non-financial information (so-called corporate responsibility reporting1). Companies have been able to follow international frameworks in their corporate responsibility reporting if they so wish.

The FIN-FSA asked audit committees whether their companies follow frameworks/standards in their corporate responsibility reporting and asked them to identify any frameworks they use (e.g. GRI, TCFD). Around 70% of respondents stated that they follow or partially follow frameworks in their current corporate responsibility reporting. The three most common frameworks/standards currently used or partially used by respondents are:

- Global Reporting Initiative (GRI)2: 77% of those who answered “yes”.

- Task Force on Climate-related Financial Disclosures (TCFD)3: 39% of those who answered “yes”.

- Sustainability Accounting Standards Board (SASB)4: 15% of those who answered “yes”.

In the new European Sustainability Reporting Standards (ESRS), existing corporate responsibility reporting standards and reference frameworks have been considered, as far as possible. The European Commission’s Questions and Answers (Q&A) provide more information on the coordination of the ESRS with other standards and frameworks, as well as on the timetable for the implementation of the ESRS.5

1 Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment and amending Regulation (EU) 2019/2088.

2 Further information is available on the website of the Ministry of Economic Affairs and Employment: https://tem.fi/en/csr-reporting

3 Further information: www.globalreporting.org.

4 Further information: www.fsb-tcfd.org.

5 Further information: https://sasb.org.

6 https://ec.europa.eu/commission/presscorner/detail/en/qanda_23_4043.